Airline Competition 1980-2010 R.I.P.

Part 3 : The numbers prove the

lack of competition

|

|

An oligopoly is when

four companies have more than 50% of the market.

Across the Atlantic, two companies have more than 50% and

four companies have 90%.

Part of a series on airline competition

- see extra articles listed in the right hand column. |

Economic textbooks are full of

the theory and explanation of how monopolies and oligopolies can

break the ideal balance between commerce and consumers, and

while economists rarely agree on much, there is close to

universal agreement that a few major companies dominating a

market is a bad thing.

Let's take the theory and see

if it applies to the airline industry as it presently is in the

US and across the Atlantic.

The Reality of Airline Market

Dominance

When is a market 'dominated'

by one (or more than one) airline(s) and when is a marketplace

fairly competitive?

We quote the

generally accepted

definitions of oligopolies and monopolies in part one of

this article series. Basically, any time four (or

sometimes more; and of course, definitely if fewer) companies

have 50% or more of a market, this is probably an oligopoly, and

if these four (or fewer) companies control more than 80% of the

market, it is most likely a monopoly (even though more than one

company is present).

US market statistics

So how do the US airlines

stack up against this measure?

Using the excellent

Bureau of Transportation Statistics, we see the following

results for US airlines :

US Market Shares, RPMs, Q3

2009

|

Rank |

Airline |

RPMs (in billions) |

Share % |

Cumulative Share |

|

1 |

Delta & Northwest |

46.5 |

21.8 |

21.8 |

|

2 |

American |

32.4 |

15.2 |

37.0 |

|

3 |

United |

27.6 |

13.0 |

50.0 |

|

4 |

Continental |

21.6 |

10.1 |

60.1 |

|

5 |

Southwest |

19.7 |

9.3 |

69.3 |

|

6 |

US

Airways |

15.7 |

7.4 |

76.7 |

|

7 |

JetBlue |

7.0 |

3.3 |

80.0 |

|

8 |

AirTran |

5.2 |

2.4 |

82.4 |

|

9 |

Alaska |

5.0 |

2.4 |

84.8 |

|

10 |

SkyWest |

3.3 |

1.5 |

86.3 |

|

|

All others |

29.2 |

13.7 |

100 |

|

|

Total |

213.2 |

100 |

|

|

The four largest carriers

have 60.1% of the total market (in terms of passenger miles

flown) and so, on the face of it, seem to be in an oligopolistic

situation.

Interestingly, if the merger

between Northwest and Delta had not been allowed to proceed, the

four largest carriers would then be AA, DL, UA and CO, with a

51.8% market share between them - right on the cusp of becoming

an oligopoly. The DL/NW merger, between the formerly

second and sixth largest carriers (as measured by passenger

miles flown) has now cemented the assumption in place that the

airline industry is oligopolistic.

The previous major merger -

between US Airways and America West - resulted in the new merged

carrier taking the sixth place on this list. There is also

a secondary measure of oligopolistic markets that looks at the

market share belonging to the eight largest competitors - so

this merger concentrated more power in the eight largest

airlines, while not affecting the market power of the four

largest airlines.

A mooted future merger

between United and Continental, should it subsequently occur,

would combine the third and fourth largest carriers, moving

Southwest up to the fourth slot, and would therefore concentrate

69.3% of the market into the top four carriers. This would

definitely tilt the market appreciably further towards being

severely oligopolistic.

The reality is worse than this

table suggests

This summary table is

however deceptively optimistic in its nature, because it

conceals within the totals lots of market pairs and lots of

cities where the market isn't split into a somewhat

oligopolistic situation with four carriers controlling 60% of

the market, and with many other smaller carriers also actively

present. As you surely know from personal experience, we

have 'fortress hubs' and strategic routes where instead of four

airlines sharing 60%, one airline alone might have 60% (or

more), creating not just oligopolistic service but near

monopolistic service for many routes.

The real scenario is that

there are lots of monopolistic markets within the broader total

US market, with some airlines controlling some monopolies, and

other airlines controlling other monopolies, such as to sort of

'average out' and, in summary, look more benign than the

underlying actuality of routes and cities.

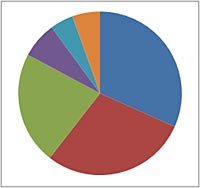

Trans-Atlantic market

statistics

Let's also look at the

international market, using DOT figures for the 12

months ended June 2009 as reported in their Show Cause order

tentatively approving the AA/BA anti-trust immunity application.

This shows the following market shares :

Market Share US-EU Market

12 months through June 2009 per DOT

|

Alliance |

Member Airlines |

Share % |

|

Star |

Austrian, bmi, Continental, LOT,

Lufthansa, SAS, Swiss, TAP, United, Air

New Zealand |

31.7 |

|

Skyteam |

Air

France, Alitalia, Delta/Northwest, KLM,

Czech |

28.9 |

|

Oneworld |

American, British Airways, Iberia,

Finnair |

22.3 |

|

- |

Virgin Atlantic |

7.1 |

|

- |

US

Airways |

4.6 |

|

- |

All

other airlines |

5.5 |

|

In this situation, where 19 airlines have collapsed themselves into three

anti-trust immune alliances, and where they hold 82.9% of the market between them

(or 87.5% if US Airways is added in with the rest of its Star

Alliance partners),

this is not just an oligopoly by all measures, but probably a

textbook monopoly (monopolies can have more than one major

player).

And so we feel sadly justified in describing this

event (anti-trust immunity being granted to the Oneworld

Alliance) as marking the death of airline competition (across

the Atlantic).

Other Factors To Test for

Oligopoly/Monopoly

The market share test we've

used in the preceding tables is a simplistic test that isn't

always completely correct, and so, in cases of doubt, economists

use some additional tests to see not only if the numbers show

there could be an oligopoly, but to confirm if companies are

indeed acting that way.

Sometimes, oligopolies can

be present when companies have smaller market shares than the

theory would suggest, other times, oligopolies are not present

even when companies have much larger market shares than needed

to cross the threshold level for oligopoly.

These tests are discussed in

detail

here and

here. To boil down the economic theory into key

bullet-point type concepts, oligopoly can be considered by

marketplace characteristics and marketplace behaviors.

The marketplace

characteristics have three main elements :

-

Small number of suppliers

who between them control most of the market : We've

spoken before about measuring markets in terms of the total

share owned by four and sometimes eight companies, but

oligopolies can sometimes have as many as about 20 different

companies, depending on other conditions.

-

Barriers to Entry :

It is difficult for new companies to enter the market.

Maybe there are huge capital investments required, long

leadtimes, legislative restrictions, limited resources, or

patent restrictions.

-

Common Product Types :

Members of an oligopoly provide similar products, perhaps

with no distinction at all (eg raw materials such as metals

and foodstuffs) or perhaps with distinction/branding but

very similar functionality (eg automobiles).

The marketplace behaviors

are

-

Interdependence :

This is a key measure of an oligopoly. The actions of

each company in the marketplace influences the market as a

whole, and will cause the other oligopolies to react/respond

- not necessarily to copy, but in some way or another to

respond. This means that each company, in choosing new

products, prices, or other changes to their activities

considers not just how the marketplace will respond but also

how their fellow oligopolies will respond.

-

Mergers and Collusion

: Because there are few companies in an oligopoly,

mergers or collusion give the companies involved substantial

extra marketplace control. Companies have a

tendency/preference to merge or collude with each other

rather than to compete.

-

Nonprice Competition :

Oligopolies would prefer not to compete on price, preferring

instead to create differentiations of products (that may be

as much illusion as reality) and to advertise and promote

their brand and products.

Think about the airlines

under these two sets of three parameters. Small number of

suppliers? Check - see the tables above. Barriers to

entry - check. Starting an airline is a time consuming

capital intensive business, needs regulatory approvals, and

needs access to scarce resources (airport gates, etc). And

all airlines, much as they pretend to the contrary, provide the

basic identical service - a flight that lasts about the same

duration, between the same cities, on the same plane, in the

same sort of seat, for the same price.

As for the second three, we

see interdependence all the time. An airline will try and

raise prices, and if the other airlines don't follow, it will

bring its prices back again. An airline will introduce a

new service (or fee) and the other airlines generally copy.

Airlines are aggressively seeking to merge or collude, either

officially with DOT permission or unofficially through backdoor

arrangements (such as alliances) and sometimes through

methodologies of dubious legality such as 'signaling' possible

price rises. Lastly, airlines attempt not to compete on

price, choosing to charge almost exactly the same fares.

Instead they choose to promote things such as their frequent

flier programs, their lounges, and - well, there's not much

else, is there.

By all of these measures,

airlines are exhibiting oligopolistic behavior.

Are Oligopolies Good or Bad

Not all oligopolies are bad.

Some can be good. The extra profit potential for a company

in an oligopolistic market can be used to fund new product

development, service enhancements, and so on (think computers

for a vivid example of this). And the large sized

companies can enjoy substantial economies of scale as a result

of their large sales volumes.

But, for reasons beyond the

purview of this article series, airlines are seldom profitable,

and in any case, even if they had excess profit to invest in

R&D, most of the need for R&D in the airline/aviation industry

lies in related fields - aircraft design and manufacture and air

traffic control in particular.

And, as discussed in the

second part of this series, the nature of the airline business

does not allow for economies of scale; indeed, paradoxically,

the bigger airlines are less efficient than the small ones.

So neither of the two main

potential benefits of oligopolies apply to the airline

oligopoly.

Let's hope the two downsides

of oligopolies also don't apply. They are a risk of

inefficiency, and a concentration of wealth and social power.

Oligopolies can be even more

inefficient than monopolies. Monopolies are more closely

subject to legislative and social scrutiny, oligopolies are less

visible so can get away with more. Many people don't even

know what an oligopoly is, thinking there to be only two types

of market - monopolistic and competitive.

As we saw in the second part

of this series, the bigger the airline (and therefore the more

it is part of the oligopolistic process) the higher its costs

and the less efficient it was (which its profits did not grow in

line with its costs/revenue). Airlines would seem to

suffer from this downside aspect of oligopolies.

As for the concentration of

wealth and social power,

this definition explains

While the concentration of wealth is not bad unto itself,

such wealth can then be used (or abused) to exert influence

over the economy, the political system, and society, which

might not be beneficial for society as a whole.

Doesn't that describe the

airlines and their very efficient government lobbying processes?

They have an amazing example to stall passenger friendly

legislation, and to draw out requirements for expensive

retrofits to their fleets proposed by the NTSB on safety

grounds.

Aren't the airlines hovering

in the 'too big to fail' category, possibly abusing the Chapter

11 process, and being subject to supportive Presidential

intervention in the past when it seemed they were about to be

impacted by labor strikes?

It seems that while airlines

have neither of the redeeming upsides to their oligopolistic

nature, they do suffer strongly from both the classic two

downsides.

Summary

The airlines meet the

classic tests for being oligopolies - both the quantitative

numerical test and the more qualitative other observations of

their characteristics and behaviors.

Although oligopolies can

sometimes bring consumer benefits, the airline tie-ups seem to

do no such thing, but rather bring out the potential downside

negative aspects of such business arrangements.

Recent merger approvals have

cemented in place the oligopolistic nature of the airlines.

Part of a series on airline competition

- please see extra articles listed at the top in

the right hand column

Related Articles, etc

|

If so, please donate to keep the website free and fund the addition of more articles like this. Any help is most appreciated - simply click below to securely send a contribution through a credit card and Paypal.

|

Originally published

12 Mar 2010, last update

30 May 2021

You may freely reproduce or distribute this article for noncommercial purposes as long as you give credit to me as original writer.

|